What is input tax credit?

Input Tax Credit (ITC) is a fundamental feature of the Goods and Services Tax (GST) system, designed to eliminate the cascading effect of taxes. By doing so, ITC helps lower operational costs, making it easier for businesses to manage their finances efficiently.

ITC allows registered businesses to claim a credit for the GST paid on goods and services purchased for business use. These purchases are often integral to expanding and developing business operations, providing necessary resources or inputs.

A key benefit of ITC is that it can offset the GST liability on the goods or services a business supplies. This means that the GST paid on inputs can reduce the tax due on outputs, improving cash flow and reducing overall tax costs for registered entities.

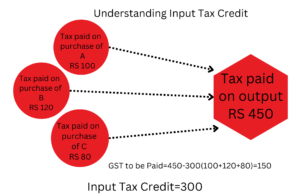

For example- you are a manufacturer:

- Tax payable on output (final product) is Rs 450

- Tax paid on input (purchases) is Rs 300

- You can claim an input credit of Rs 300 and deposit only Rs 150 in taxes

Here is a link to the official document from GST Council – View here

Who can Claim Input Tax Credit Under GST?

ITC claims can be made by any registered person. It is claimable on the inward supply of goods and services or both

- The dealer must possess a valid tax invoice.

- The goods or services must have been received.

- GST returns must be filed.

- The supplier must have paid the tax charged to the government.

- If goods are received in instalments, ITC can only be claimed upon receiving the final instalment.

- No ITC is permitted if depreciation has been claimed on the tax portion of a capital good.

Time Limits for Claiming ITC Under GST

The time limit for ITC claims under GST is one of the given two dates, whichever is earlier:

- The due date to file the annual return for that financial year or

- 30th November of the following financial year to which such invoice pertains.

For example, ideally, an individual can seek an ITC claim for FY 2022-23 before filing the October 2023 return or the annual return for FY 2022-23, whichever is earlier.

How to Claim Input Tax Credit (ITC) Under GST?

To claim Input Tax Credit (ITC) under GST as a registered individual, follow these steps:

- Verify ITC Details Using GSTR-2B: GSTR-2B is an auto-generated statement reflecting the returns filed by suppliers. Use it to verify your ITC details.

- Match ITC with Your Records: Reconcile the ITC recorded in your books with the invoice-wise details in GSTR-2B to ensure accuracy.

- File GSTR-3B: Declare the matched output tax liability and ITC details in your monthly GSTR-3B return.

- Resolve Mismatched ITC with Suppliers: If any discrepancies arise, follow up with suppliers to correct mismatches.

- Reconcile and Claim Adjustments: Reconcile any differences and include them in the ITC claim for the following month’s return.

- Reverse Excess ITC with Interest: If any excess ITC was claimed, ensure it is reversed with applicable interest.

Claiming ITC helps reduce the tax burden and allows a smooth credit flow under GST. By following these steps and adhering to ITC rules, businesses can leverage GST benefits, improving cash flow and profitability.

Documents Required for Claiming Input Tax Credit (ITC) under GST

Here’s a list of essential documents required for claiming input tax credit claim ITC under GST

- Invoice from Supplier: A valid invoice issued by the supplier for the goods or services provided.

- Debit Note from Supplier: If applicable, a debit note is issued by the supplier to the recipient.

- Bill of Entry: Required for imported goods, documenting customs clearance and duties.

- Special Invoices for Reverse Charge or Low-Value Transactions: In cases where a reverse charge applies or for amounts below Rs. 200, a bill of supply or specific invoice as per GST rules must be provided.

- Invoice or Credit Note from Input Service Distributor (ISD): Any credit note or invoice issued by an ISD, following GST invoice regulations.

- Bill of Supply from Supplier: A bill of supply issued by the supplier of goods, services, or both.

Keeping these documents organized and readily accessible ensures a smooth ITC claim process and maintains compliance with GST regulations. For more details on claiming ITC, visit our comprehensive guide on MSMESTORY.

Reversal of Input Tax Credit (ITC) under GST

Input Tax Credit (ITC) under GST is allowed only on goods and services used strictly for business purposes. ITC cannot be claimed if these are used for personal or non-business purposes, or to make exempt supplies. Additionally, certain scenarios require the reversal of ITC already claimed:

- Non-Payment of Invoice within 180 Days: If an invoice remains unpaid for over 180 days from its issue date, the ITC related to that invoice will be reversed.

- Credit Note Issued to Input Service Distributor (ISD): If a credit note is issued by a supplier to the Head Office (ISD), any reduced ITC must be reversed accordingly.

- Inputs Used Partially for Personal Use or Exempt Supplies: For businesses using inputs partially for business and partially for personal use or exempt supplies, ITC on the non-business portion must be proportionately reversed.

- Capital Goods Used Partially for Personal Use or Exempt Supplies: Similar to inputs, if capital goods are used partly for personal purposes or exempt supplies, the ITC on this portion must be reversed.

- Under-Reversed ITC After Annual Return: After filing the annual return, if the actual ITC reversal for non-business or exempt purposes is less than required, the difference will be added to the output tax liability, with interest applicable.

These ITC reversals must be reported in GSTR-3B. For more insights on correctly managing ITC reversals and calculating ITC for mixed-use goods, explore our in-depth guide on MSMESTORY. Proper ITC management ensures GST compliance and reduces tax liabilities for businesses.

ITC Reconciliation under GST

Input Tax Credit (ITC) reconciliation is a vital process for businesses under the Goods and Services Tax (GST) regime. It involves matching the ITC claimed in the taxpayer’s purchase records with the details provided by suppliers in their GST returns. This process ensures accuracy in ITC claims, prevents discrepancies, and avoids interest or penalties due to mismatches or errors.

Why ITC Reconciliation is Important

The main objective of ITC reconciliation is to verify that the ITC claimed is genuine and matches the data filed by suppliers in their GSTR-1 forms. When businesses purchase goods or services, the GST paid on these transactions is eligible for ITC, provided it aligns with the supplier’s records. Discrepancies can arise when suppliers fail to report transactions, report incorrect details, or file returns late, causing issues for buyers claiming ITC. Regular ITC reconciliation also ensures smooth cash flow, as businesses can claim only the correct, eligible ITC, thereby reducing overall tax liability.

How ITC Reconciliation Works

- Matching ITC Claimed with GSTR-2B: GSTR-2B, an auto-populated statement, provides details of ITC available based on supplier records. Businesses use it to match the ITC claimed in their purchase register with what’s reported in GSTR-2B.

- Identifying and Resolving Discrepancies: If there are mismatches between the business’s records and GSTR-2B, the business must coordinate with suppliers to ensure they correct errors in their returns. This helps avoid ITC disallowances or penalties.

- Reporting ITC Adjustments in GSTR-3B: Businesses should declare reconciled ITC details in their GSTR-3B monthly return, making adjustments for mismatches identified during reconciliation.

Best Practices for Effective ITC Reconciliation

- Perform Monthly Reconciliation: Regularly reconciling ITC, ideally each month, helps address issues before they accumulate.

- Follow Up with Suppliers: Promptly addressing mismatches by coordinating with suppliers ensures timely corrections.

- Maintain Comprehensive Documentation: Detailed records support ITC claims and help verify compliance with GST regulations.

Effective ITC reconciliation promotes compliance, prevents cash flow interruptions, and allows businesses to maximize their tax benefits under GST. For assistance in ITC reconciliation and seamless GST compliance, MSMESTORY provides expert guidance and resources tailored for businesses.

Special Cases of Input Tax Credit (ITC) under GST

Understanding special cases of ITC under GST is essential for businesses to claim credits accurately and comply with GST regulations. Here’s a breakdown of the key scenarios for ITC claims:

-

- ITC on Capital Goods

ITC is available for capital goods used for business purposes. However, ITC cannot be claimed if:- The capital goods are used exclusively for producing exempted goods.

- The capital goods are used solely for non-business (personal) purposes.

- ITC on Capital Goods

Note: No ITC can be claimed if depreciation is charged on the tax component of these capital goods.

-

ITC on Job Work

A principal manufacturer can send goods to a job worker for further processing, retaining eligibility for ITC. For example, a shoe manufacturer may send semi-finished shoes to a job worker for additional work, such as sole fitting. In this scenario, the principal manufacturer can claim ITC on the tax paid for these goods sent for job work.

ITC is available for goods sent to a job worker in both cases:

- When sent from the principal’s business location.

- When sent directly from the supplier to the job worker, goods sent for job work must return to the principal within 1 year (or 3 years for capital goods) to retain ITC eligibility.

-

ITC from Input Service Distributor (ISD)

An Input Service Distributor (ISD) can be the head office, branch, or registered office that collects ITC on purchases and distributes it to various branches. ITC distribution is done under separate heads, such as CGST, SGST/UTGST, IGST, or less, based on the nature of the services received and the branch’s location.

-

ITC on Business Transfers

During mergers, acquisitions, or business transfers, input tax credit available to the transferor can be transferred to the transferee. This enables the successor entity to benefit from the Input Tax Credit accumulated before the business transition.

Navigating special ITC scenarios ensures compliance and maximizes tax savings. For more information on ITC and GST compliance, explore expert resources at MSMESTORY.